The Missing Link in Law Firm Financial Performance

Law firms generate more financial data than most industries: billing, collections, realization rates, A/R aging—it’s all tracked. Yet most firms can’t answer a deceptively simple question:

How efficiently does work turn into cash?

That gap between data richness and operational insight is where firms quietly lose both time and revenue.

The Problem with Period-Based Reporting

Traditional law firm financial reporting is organized around accounting periods, not around the lifecycle of work. Hours are recorded when performed. Bills go out when time is processed. Cash is recognized when payments arrive. Each view is accurate. But none of them are connected into a single revenue story.

The result is a fundamental blind spot. A strong collections month may simply reflect invoices issued many months prior. A billing spike may mask a growing backlog of aged WIP. Without a throughline connecting work performed → billed → collected, firms end up managing lagging indicators instead of the process that drives them.

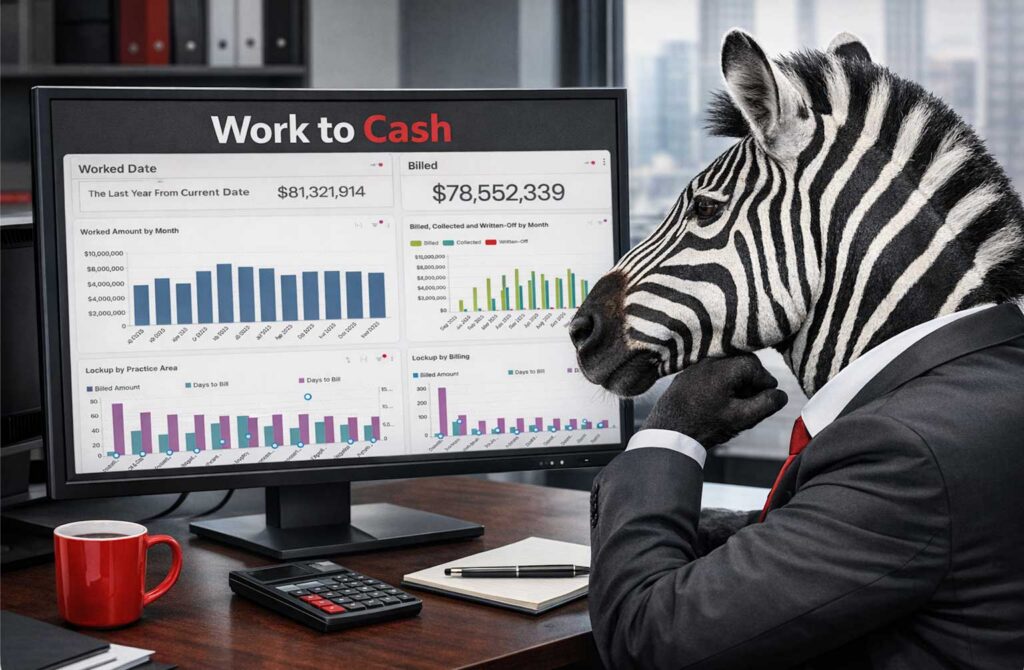

The alternative is cohort-based analysis: organizing financial data around when work was performed and following through to when that work was billed and collected. When you take all time recorded in a single period—say June—and trace what happened to it, a very different picture emerges. You can see how long it took to become an invoice, how long that invoice sat before payment, and what percentage of the original value was ultimately collected.

This reframing shifts the question from the useful“How did we perform this month?” to the predictive “How efficiently is our revenue engine actually running?

When you take all time recorded in a single period—say June—and trace what happened to it, a very different picture emerges.

Three Phases, Three Failure Points

A work-to-billed-to-cash model breaks the revenue cycle into three distinct phases: each with its own cycle time and its own risk profile.

Worked to Billed

This is the elapsed time between when an hour is recorded and when it appears on an invoice. For many firms, this runs longer than partners realize: often 30 to 60 days, and sometimes significantly more. Delays here stem from slow time entry, billing review bottlenecks, or partner reluctance to close out matters. Every day of delay is a day of unnecessary lockup, and it compounds: slow billing tends to correlate with higher write-off rates, because aged WIP is harder to defend and easier to discount.

Bill to Cash

Once an invoice is issued, the clock starts on collections. This phase reflects a mix of factors: client payment behavior, invoice clarity, and the effectiveness of follow-up. Benchmarks vary, but firms with median A/R cycle times consistently above 90 days should ask a harder question: is this client behavior, or process friction?

Leakage

This is where value disappears. Pre-bill write-downs, post-bill adjustments, and disputed invoices each represent work performed that never converts to revenue. Leakage is often tracked at the firm level as realization rate—but that aggregate obscures where it actually occurs and whether it’s predictable.

Lockup Isn’t a Metric. It’s a Diagnostic Tool.

Most firms track lockup — the combined capital tied up in WIP and A/R — as a firmwide metric. That number matters, but it doesn’t tell you much on its own. When you break lockup down across three dimensions, patterns that drive action start to emerge:

Practice Area

Some practices bill slowly by convention; others collect slowly because of matter complexity or client norms. Understanding which practices are structural outliers versus which are underperforming relative to peers is a necessary distinction before any intervention makes sense.

Billing Attorney

Individual behavior is often the most significant driver of WIP cycle time. Some partners move work through the billing process quickly and consistently; others hold WIP for reasons ranging from perfectionism to avoidance. Visibility creates accountability, and when attorneys can see their own cycle times benchmarked against peers, behavior tends to change.

Client

Payment behavior is not uniformly distributed. Some clients are reliably slow; others are dispute-prone in ways that correlate with specific billing patterns. Identifying these clients early—ideally before they age into problem A/R— allows firms to adjust billing practices, set expectations proactively, or make informed decisions about engagement terms.

This multidimensional view transforms lockup from a static financial metric into a diagnostic instrument. Instead of concluding that “lockup is too high,” you can identify specifically where it’s accumulating, why, and what to do about it.

The Bottom Line

Law firms don’t have a revenue problem.

They have a conversion problem.

The work is being done. The value is being created. But without clear visibility into how that work flows through billing and into cash — and without the ability to measure cycle times, diagnose bottlenecks, and identify where value is being lost — firms are managing outcomes rather than the process that produces them.

Worked-to-billed-to-cash analysis closes that gap. It connects the dots that period-based reporting leaves disconnected, and it gives finance leaders the framework to move from describing what happened to understanding why and what to do about it.

That’s where financial reporting stops being descriptive and starts becoming strategic.

Law firms don't have a revenue problem. They have a conversion problem.